.jpg) |

| Oh wait, that was the TSA |

Many people think that they can "time the market;" that is, sell stock when it's high and buy at the bottom of a crash, when prices are lowest and you can buy more shares.

.jpg) |

| Like so |

In an ideal world, that would work, and we'd all be rich. In reality though, people's emotions get the better of them and they tend to think rising stocks will continue forever (or that the crash will continue forever and you'll be left penniless). Just look at the sub-prime housing crisis of the 2000s.

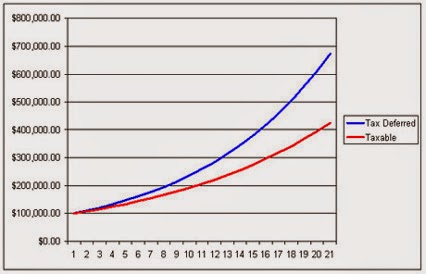

It's difficult to time the market. What really matters is not timing the market, but rather time in the market. The earlier you start saving and investing, the better off you'll be. Einstein may or may not have once said that compound interest was the strongest force in the universe. Check out the difference a few years can make. The person on the left invested $5000 a year from age 25-35 and stopped contributing after that, and the person on the right invested the same amount for 25 years, and still ended up with less than the 25 year old.

|

Now, I'm not saying that there aren't people who can outperform the market. Almost one in five does. I'm just saying that chances are, you (or the fund manager that convinces you to let them handle your money) won't be one of them.

|

Statistically, your best bet isn't to try to outperform the market, but give yourself every advantage you can by reducing fees. Many actively managed mutual funds have annual fees of a percent or two. That is, for every $1000 you have in the fund, they will take out $10-$20 annually. Not of what you earned over the year, but of the entire amount. Even if you lost money.

Now we come to the whole point of this article. The TSP charges 0.02% annually. That's twenty cents for every thousand dollars invested. That's virtually non-existent. So if you're not doing so already, fund your TSP. Put away as much money as you possibly can, and future you will thank present you for it. Fees aside, a 401k plan (or TSP in this case) is tax-deferred. That is to say, you won't pay taxes on money you put in until you retire. That gives you an extra 15-35% (depending on your tax bracket) that you can have earning money for you. Let's pretend you make $50,000, and put in the 2015 maximum of $18,000. Not only are you paying taxes on just $32,000, but you're in a lower tax bracket, AND saving more for down the road.

The tone of this article may suggest that you should buy and hold forever. I am not actually suggesting that. Regular checkups (maybe once a year) are in order. There is some buying and selling that needs to be done, and re-weighting of your portfolio. That means that if you have your net worth divided up evenly (25% each) between US stocks, international stocks, bonds, and precious metals, after a year of stock market fluctuations, the allocation is going to be different. That's when you sell any excess in one area and put that money in the portion that went down. For example, if US stocks now represent 35% of your portfolio (up from 25% a year ago), and your bonds are at 15%, you sell 10% of stocks, and use that money to buy more bonds, bringing balance back to the Force.

The TSP has several funds. Unless you specify otherwise, your contributions will go into the G Fund, which doesn't really earn you anything, but never goes down, so it's great during a recession. The best site I've found so far for the TSP is called TSPallocation.com. The author has done his research and switches his money between the funds depending on what phase of the business cycle we're in. There's a lot of financial mumbo jumbo you're probably not interested in, but he has his current recommendation right at the top of the page, so I'd suggest a visit right after funding your TSP.

EDIT: If you have another job outside of the military, say you're in the National Guard and make like $5,000 a year, you can also have a 401k with your other job. In this case, I would suggest putting all of your military money ($5,000) into the TSP, and then funding your 401k with the rest of the maximum contribution (18,000 - 5000 = 13,000) into the 401k. Then start funding your Roth IRA, only after you've maxed out your TSP/401k.